| This is all relative to packer capacity or willingness to harvest cattle six days out of the week. But the recent two weeks have also featured very healthy harvested head count

totals. The 668K head total seen the week of October 25 is very near the perceived upper-end of the range for weekly capacity for the industry. There are very few weeks in the past five years equaling or surpassing that number.

Reports early this week indicate that feedyards have upped their bids to the $132 to $134/cwt. level, but packer bids are at $130/cwt. with little trade developing. The premium in the north has re-emerged, with packers seeking higher grading cattle to fulfill holiday demand.

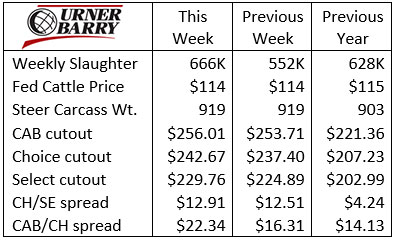

Demand for boxed beef pulled carcass cutout values slightly higher last week, as prices increased for CAB and Choice products. Early this week the Select price narrowed the gap on Choice, but the spread is quite wide as a starting point. CAB traditional, CAB Prime and USDA Prime carcasses are all in high demand and the price spreads show this.

With cutout values relatively steady, the adjustments across the carcass are subtle. It looks like ribeyes have ticked a bit higher with the return to holiday demand buying. Strip loins are

seeing an uptick, rightfully, as they are becoming a focus of buyers, with the price spread between ribeyes and strips historically wide in recent data.

A practical look at cutout values suggests that fourth-quarter demand is firm at this time. The market will likely see a cooling period just ahead of Thanksgiving, with retail focus momentarily shifting to turkeys.

|