|

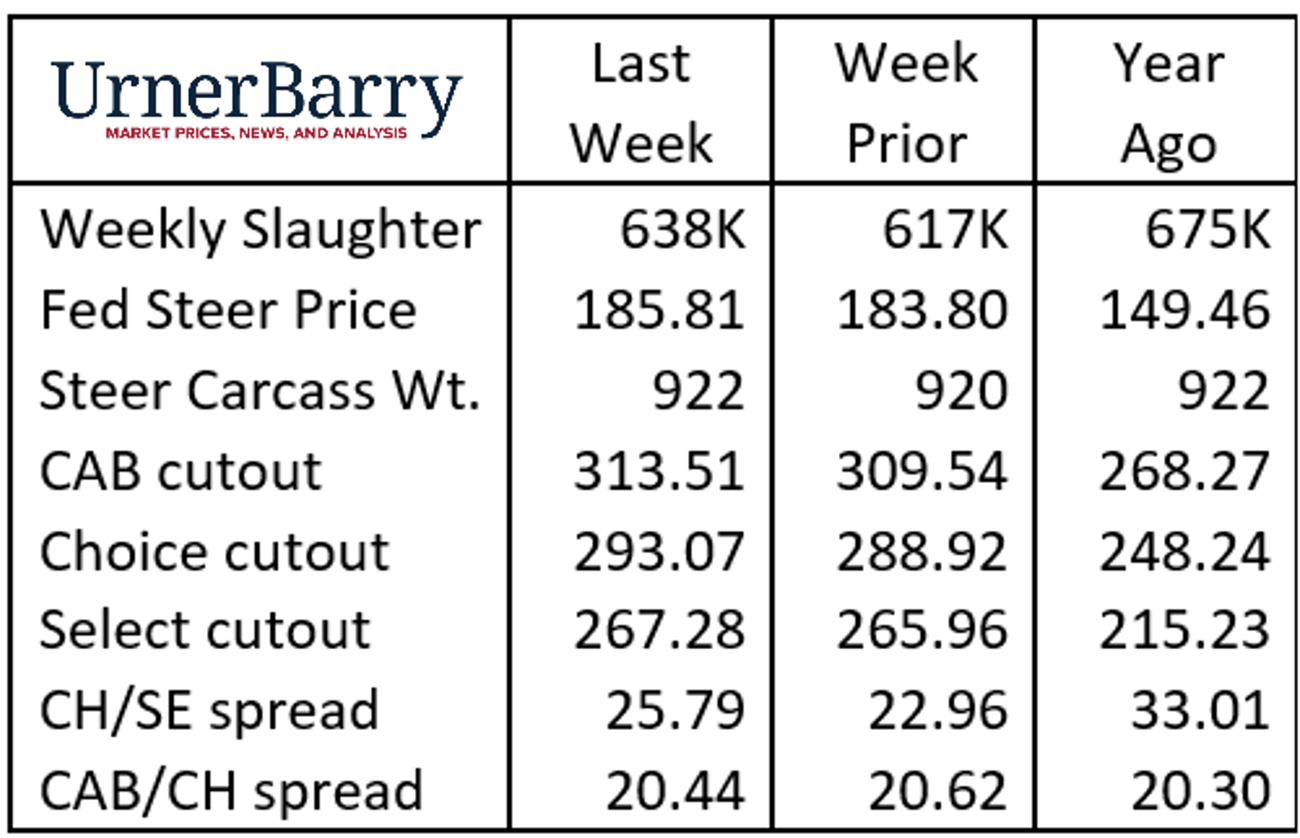

The October 1 Cattle on Feed report, published last Friday, is the most impactful short-term market factor at this time. Feedlot placements for September were unexpectedly 106% of placements a year ago, contrasted against varied analyst pre-report estimates for placements just over 100%. December Live Cattle futures, which closed Friday at $184.60/cwt., ended Monday’s session at $178.35/cwt., a $6.25/cwt. decrease). In a volatile, short-term scenario, Live Cattle contracts began to recover some of the lost ground by Tuesday morning.

Meanwhile, current cattle and beef market fundamentals are positive. Packer demand for cattle was sharp last week with the $2/cwt. price increase on a significant volume of negotiated cattle. Total USDA Choice carcass production is 8% lower than a year ago in the latest weekly report, driven lower by a one percentage point decline in the Choice grade.

Also, cutout values have turned the corner with higher weekly average values across the board last week with CAB up $3.97/cwt., and Choice up $4.15/cwt. and Select $1.32/cwt. higher. As we had mentioned two months ago, the dip in total USDA Choice boxed beef tonnage was destined to hit the fourth quarter market with widening Choice-Select price spreads. That is evident in our latest data with the Choice cutout $25.79/cwt. premium to Select. The CAB/Choice price spread is more stable at $20.44/cwt., which is historically wide but perfectly aligned with October price spread values since 2020.

|