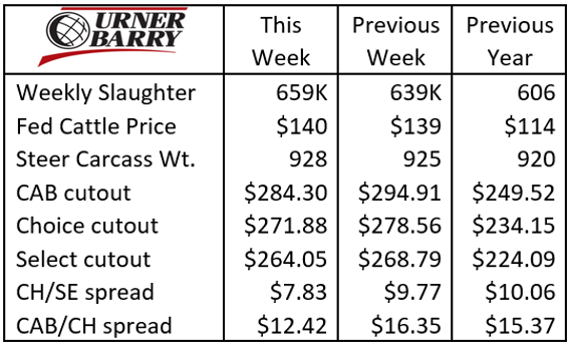

| Carcass weights are back on the rise, with the most recent 928 lb. steer carcass weight reaching back up to touch the early Jan. high. Despite some true winter weather in the

northeast and southern feeding regions, there is a vast area of dry and temperate conditions in the high plains with good conditions that continues to push weights higher. Additionally, in the month of Jan. we failed to harvest about 100K head of cattle that “could have” been slaughtered, had labor issues not plagued the industry again with further COVID ramifications.

The wholesale beef market was firmly lower last week with some items touching 52-week price lows. The most valuable middle meat cuts, ribeyes and tenderloins, led the downward price decline. CAB brand tenderloins have declined from $14.50/lb. in mid-January to last week’s $11.80/lb. market

average, the most dramatic decline in that period since 2007. The difference, of course, is the record-high recent Jan. price prior to the drop. Strip loins and top butts are on an increasing price trend and will likely only see a brief pullback as we move toward the spring demand period.

Economic inflation continues to be a headline and concerning to the beef marketplace. However, if weekly slaughter numbers continue to show the kind of improvement seen last week then there is hope for beef end users that larger production can support lower wholesale prices.

|