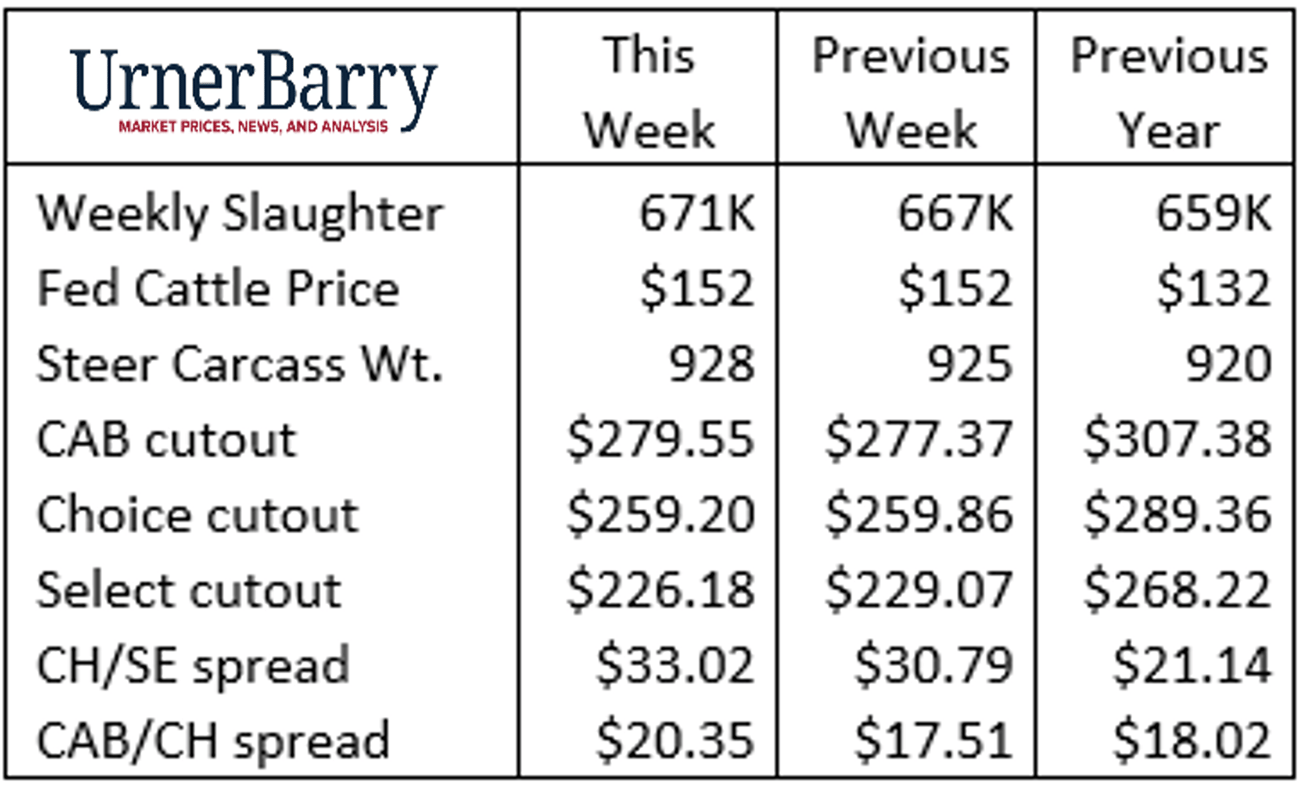

| The current cattle markets can provide a history lesson for those new to the scene. With last week’s $152/cwt. fed cattle average, feedyards experienced the highest price since June 2015. To give a quick recap of that era: record-high prices, fueled by a supply chain starved for cattle numbers, came to an abrupt end. The November 2014 record steer price of $171/cwt. eroded rapidly and bottomed out 9 months later in September 2015. Following the 31% drop to $117/cwt., the market stabilized and turned higher. This signaled the end of tight cattle supplies, caused by drought liquidation, and beef cattle producers were able to restock the nation’s cow herd.

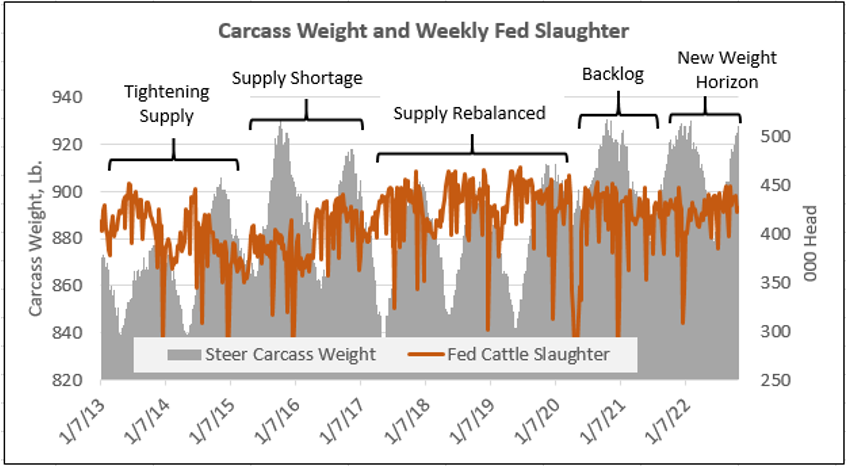

At the market high in November 2014, weekly steer/heifer slaughter head counts were near 445,000 head, just 13% smaller than the average in the most recent four-week period. At the 2014 market high, carcass weights averaged 874 lb. whereas most recent carcass weights in 2022 have

been 18 lb. heavier at 892 lb. The resulting estimated carcass tonnage is 15% larger in recent weeks than in November 2014.

It’s interesting to note that while fed cattle prices declined precipitously in 2015, weekly slaughter head counts continued to trend lower in 2015 as well. As a matter of fact, fed slaughter was 4.8% smaller in 2015 than the prior year even as price declined at three times this pace.

|