| Focusing on fed cattle slaughter, the past four Saturdays have averaged just 7,500 head, in keeping with the latest pattern. In the past four Fridays, harvested head counts

ranged from 71% to 95% of the weekly Monday through Thursday daily averages.

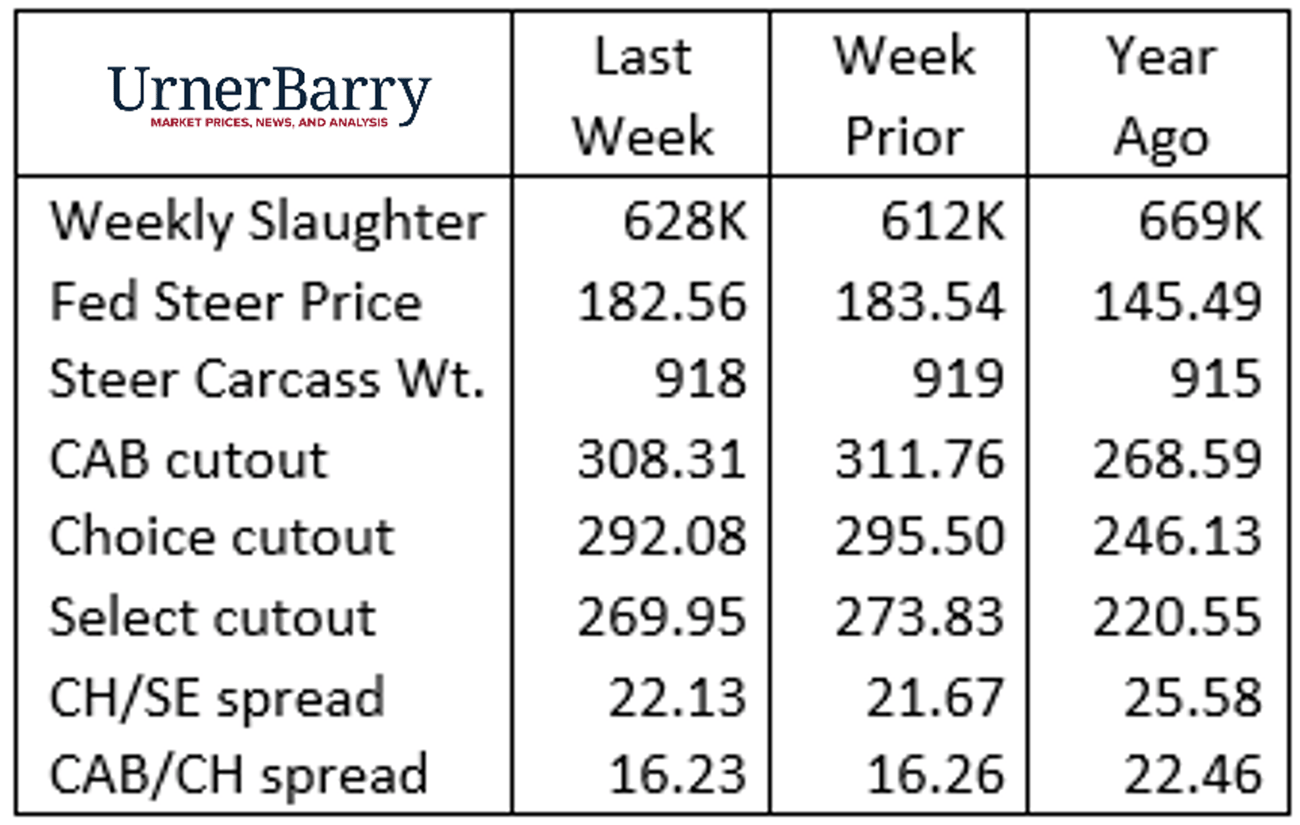

CME Live Cattle contract price volatility has been the overriding factor tempering spot cash cattle values most recently. The threat and subsequently averted government shutdown jostled equity markets and this volatility spilled over into commodity markets. The October LC contract has traded in a wide range from $186/cwt. to as low as sub-$182/cwt. in the past eight trading days. Futures are leading the market during this period but the spot market stands to move to the front as the fourth quarter continues.

The total beef market complex awaits a turning of the tide as anticipated

fourth-quarter demand has historically turned boxed beef values upward in the second half of October. The waiting will commence this week as Urner Barry’s carcass cutout values this Monday showed a $3.02/cwt. decline in the Choice cutout price to mark $288.75/cwt.

Reviewing carcass cutout prices shows many cuts are priced according to the seasonal playbook. Chuck and round items are priced steady to slightly higher as consumers look for lower-cost cuts. As well, cooler weather in many regions signals increases in roasting items.

Strip loins and shortloins are capturing attention as buyers see value in these items that have adjusted to much lower prices. Tenderloins

won’t offer such an opportunity as stout fourth quarter demand lies ahead and early demand already has CAB tenderloins priced over $15.00/lb. wholesale. Ribeyes recently priced lower for a few weeks but the small share available on the spot market should now price higher into early December.

Thin meats have come well off of their summer highs and are being picked by buyers. Similarly, CAB grinds showed weakness in last week’s pricing but remain at historic highs.

|