| A broader view of fed catttle prices for January reveals a sideways price trend, with very little tie from boxed beef values to fed cattle prices.

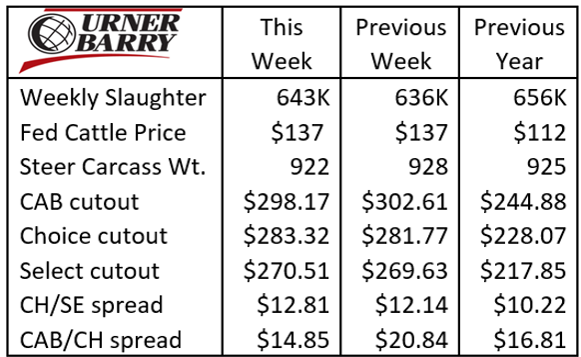

Packer efficiency improved last week, with an incremental uptick in the slaughter pace to 643K head, a 1.1% increase over the prior week. As we’ve reiterated many times before, larger slaughter rates are key to the success of every supply chain sector. There is no downside to larger head counts at this time.

The historical bias for beef demand for the month of February is lower. As a matter of

fact, Feb. tends to be the low-demand month of the year. We can practically throw this aside in 2022 because of the smaller harvest pace.

Beef inflation is a two-pronged anomaly today. Of course, the broader economy is reflecting the inflationary conditions across all consumer goods. Yet retail beef prices continue to bear the added burden of the imbalance in supply and demand.

Boxed beef values last week were mixed, with the CAB cutout reported slightly lower but Choice and Select values a bit firmer. Early this week, the daily pricing shows a softer pricing trend across the board. Two primary factors are continued concerns of COVID and the fact that current retail beef price levels are record high for this time of the year, 20% higher than the same period last year. Regarding COVID concerns, end users are likely debating that normal Valentine’s Day beef demand will be lessened.

|